Average student loan payments to top $200 once resumed

Canva

Average student loan payments to top $200 once resumed

Young person sits in living room looking over bills.

Millions of student loan borrowers will soon be adding a monthly student loan payment on top of the other household bills like credit cards and car loans. On pause since March 13, 2020, federal student loan payments will resume on the first day of October 2023, with interest accrual restarting in September.

The Biden administration’s plan to cancel some or all of the student debt of millions of borrowers was overturned by the Supreme Court on June 30, 2023, though the president said in the wake of the court’s decision that he’s taking a look at different plans to approach the issue again.

In this analysis, Experian explores what monthly payments will be like for many borrowers once repayment resumes, as well as some new approaches to student debt relief programs.

![]()

Experian

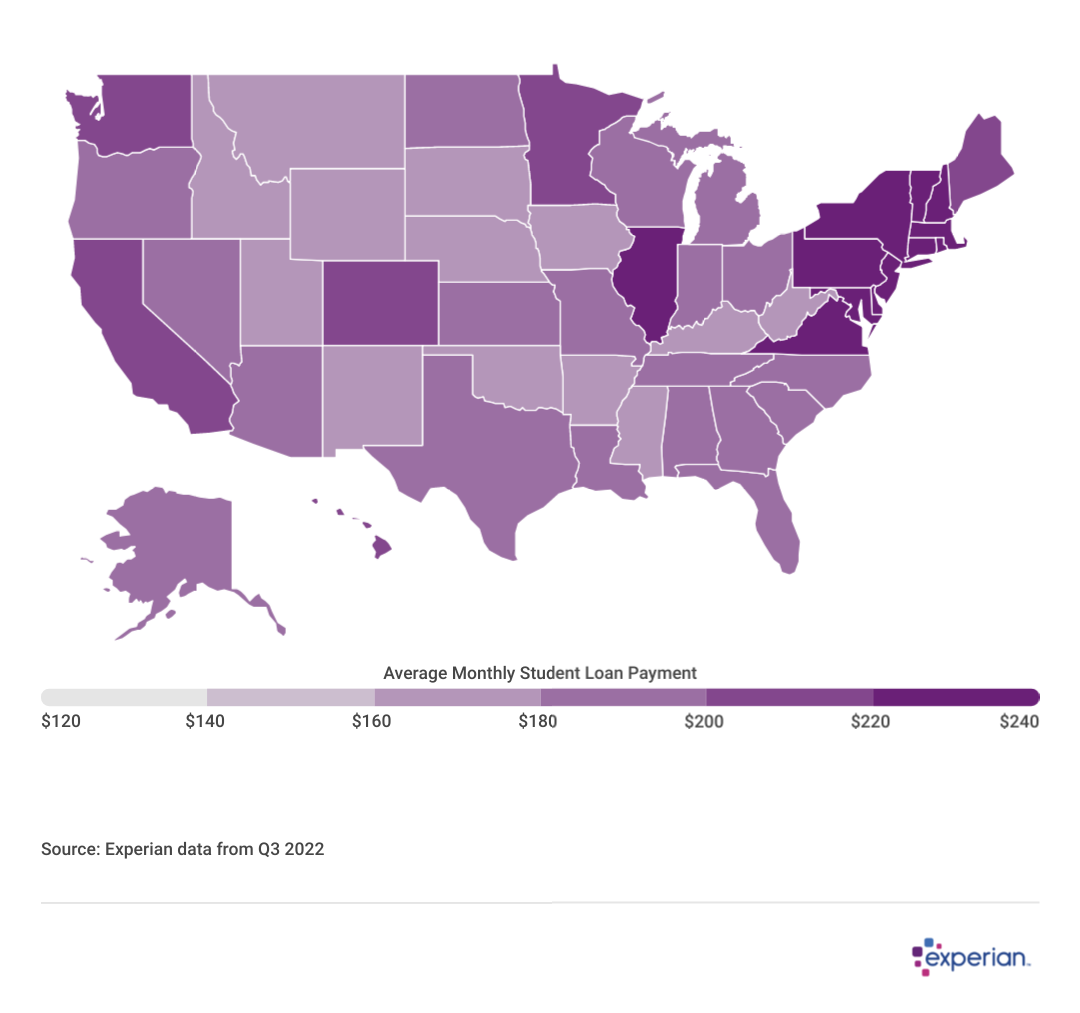

The Average Monthly Student Loan Payment Is $203

United States heatmap showing average student loan payments per state.

Student loan borrowers will start to make an average payment of $203 later this summer toward their student loan balances, according to a data analysis by Experian, assuming no further reductions in the average due to student loan forgiveness. And while that’s not as much as most car loan payments these days, it’s yet another financial obligation for consumers who are already dealing with higher costs across the board due to inflation.

It’s difficult to imagine a good time for a new large monthly bill to arrive for most consumers, but 2023 certainly isn’t it. Consumers are already fighting inflation—especially for rental and home costs—as well as higher interest rates for loans and credit cards. Both these factors are already eating into the savings people amassed over the past few years. One silver lining: Unemployment rates remain low, so fewer consumers are experiencing disruptions in income.

Experian

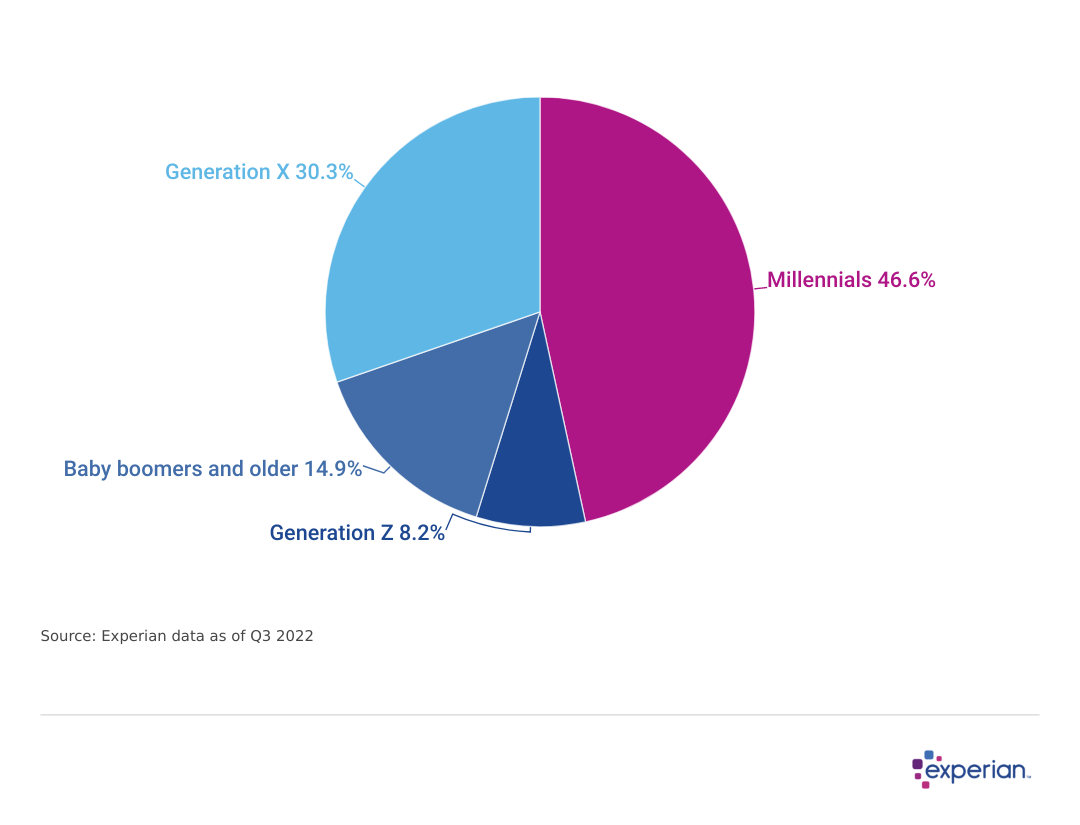

Renewed Student Loan Payments Will Add to Already Growing Household Debt Burden

A pie chart showing that 46.6% of millennials will have student loan payments resume.

Household debt is growing at its fastest pace in 20 years. Higher interest rates on some of that debt, like credit cards, ensure that households may face continued pressure in paying their debts throughout the remainder of 2023.

Among all generations, the percentage of household income that’s devoted to debt repayment remains steady, Federal Reserve data shows. And while this so-called debt service ratio isn’t rising overall, it is rising for some borrowers and falling for others. Most student loan borrowers are millennials, and their expenses generally rise as they age. Meanwhile, older consumers are less likely to be burdened as much by loan and mortgage payments.

Crucially, student loan payments will impact younger borrowers even more when they resume. Millennials carry nearly half of outstanding student loan debt in 2023, making them the generation that stands to bear the brunt of resumed student loan payments.

Student Loan Borrowers on Pause Improved Their Credit Scores as Much as Other Consumers

Consumers with student loan debt in 2022 have slightly lower average credit scores than the population at large, according to the study. As of the third quarter (Q3) of 2023, the average FICO Score of a student loan borrower was 693, somewhat lower than the national average FICO score of 714. However, the current average score among student loan borrowers is 11 points higher than it was in 2019—roughly the same growth experienced by those without student loans.

Two factors inform the 20-point FICO Score difference between student loan borrowers and the general population. One is the demographic difference: Most student loan borrowers are under 40 years of age (although older borrowers with student loan balances are becoming more common). And while age isn’t a factor in calculating one’s credit score, the length of one’s credit history is, and longer histories are beneficial. For the most part, student loan borrowers carry and repay balances when their credit history is still in its early stages.

The second reason for lower scores among student loan borrowers is the financial burden many student loan borrowers continue to carry, even after a three-year payment pause on their loans. And although most student loan borrowers were current on their loans prior to the initial student loan pause in 2020, delinquencies and defaulted loans are greater for student loans than any other type of consumer loan. As making on-time payments is crucial toward maintaining and improving one’s credit score, the relatively higher delinquencies and defaults among student loan borrowers ultimately translate to lower average FICO Scores for these consumers.

Other Offramps for Student Loan Borrowers

The Supreme Court ruled against the loan forgiveness of up to $20,000 for those making under $125,000, but borrowers can consider other approaches to help lower some of their balances, including new programs announced by the federal government following the decision.

- Public Service Loan Forgiveness programs have quietly accelerated the pace at which they’ve been granted. Currently, more than 500,000 loan borrowers received loan forgiveness, with the average loan size exceeding $68,000—many times the $10,000 or $20,000 offered to some borrowers last August. It’s possible that this program expands its reach in upcoming months.

- Workplace student loan benefit programs were already beginning to take root in U.S. corporations before the student loan pause took effect in 2020. When payments resume, there’s reason to think more employers, eager to attract and retain workers, will begin to offer loan repayments as a workplace benefit—something only 7% of companies offer today. Aside from the obvious financial relief, these corporate benefits can also reduce some of the administrative headache of paying back loans, including, in some cases, making the payment directly to the loan servicer—a point of friction for some student loan borrowers.

- Income-driven repayment plans are a collection of repayment plans that are keyed toward the income of the student loan borrower. They generally cap repayments based on a percentage of a borrower’s income. Prior to the court’s decision, there were four types of income-driven plans. Following the ruling, the U.S. Department of Education announced another new income-based repayment plan called Saving on a Valuable Education (SAVE), which the administration states will reduce monthly payments to zero for low-income borrowers, capping undergraduate loan repayment at 5% of discretionary income.

- A new 12-month transition period is designed to help borrowers restart loan repayments and avoid delinquency or loan defaults. In a statement released June 30 in the wake of the Supreme Court decision, Education Secretary Miguel Cardona encouraged borrowers to continue making payments during this grace period if they’re able to, since interest will continue to accrue.

With payments (and interest) paused throughout the pandemic, the total balance of outstanding student loan debt has declined slightly from its peak of $1.59 trillion in September 2021, according to the study. Programs and benefits like those listed above may drive down total outstanding student loan balances even further, independent of the Supreme Court decision in June.

Methodology

The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of the company’s consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.