20%, 10% or 5%? How your down payment affects the rest of your finances

Canva

20%, 10% or 5%? How your down payment affects the rest of your finances

A couple carrying boxes moves into a new home.

When interest rates were low and stocks were on a tear, the demand for American homes pushed prices to unprecedented heights. Down payments have also risen, but the median down payment of 14% is still well below the traditional standard of 20%. But with different associated costs, like PMI and higher mortgage payments, smaller down payments raise the issue of opportunity costs.

SmartAsset crunched the numbers to find the overall costs – and opportunity costs – of putting down 20% vs. 10% vs. 5% on a home in today’s environment. While mileage may vary with frequently changing interest rates, it turns out there are pros and cons to all three approaches. One strategy, however, is the clear winner when it comes to overall savings.

![]()

SmartAsset

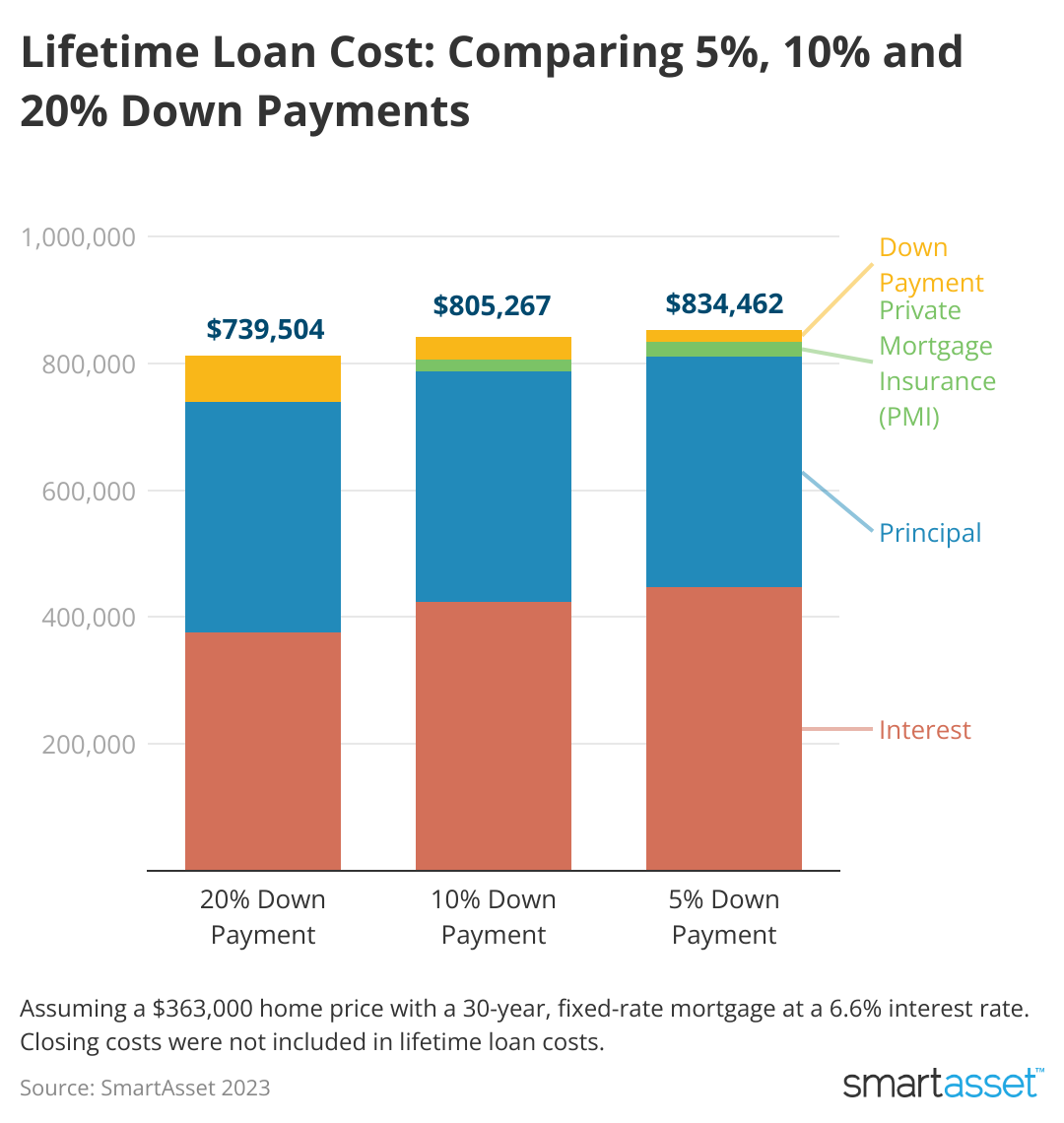

Let’s Compare Three Down Payment Sizes

A bar chart compares the lifetime costs of three similar mortgages with different down payments.

Imagine three people with identical budgets all set out to purchase homes. The three buyers have enough savings to put 20% down on their homes, but only one takes that route. The other two buyers make smaller down payments and invest their remaining cash in the stock market.

Here’s a closer look at these buyers:

- 20% Henry: Henry makes a full 20% down payment but has no money left over to invest.

- 10% Tanya: Tanya makes a 10% down payment and invests the remaining cash in the stock market.

- 5% Frank: Frank only puts 5% down, which leaves him with the most money to invest in the stock market.

How much Henry, Tanya and Frank end up paying over the course of their 30-year mortgages is based on the following assumptions:

- Home price: All three buyers purchase a home for $363,000 – the median sales price of existing homes.

- Interest rate: Each buyer pays a 6.6% interest rate on their loan, the national average for a 30-year fixed-rate mortgage.

- PMI: Frank and Tanya both put less than 20% down, so they’ll pay private mortgage insurance (PMI). This monthly surcharge automatically goes away once their home equity reaches 22%.

- Rate of return: Tanya’s and Frank’s investment portfolios will grow at an average rate of 7.9% per year – the average rate of return for 60/40 portfolios over the last 30 years. Those returns compound monthly for 30 years.

SmartAsset

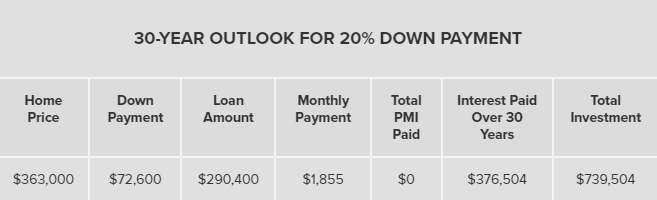

Henry’s Approach: Put Down the Full 20%

A table showing various aspects of a mortgage with a 20% down payment.

By opting for a 20% down payment ($72,600), Henry will pay less interest and avoid PMI, resulting in lower monthly payments than Tanya and Frank. After 30 years of making regular monthly payments, Henry will have spent a total of $739,504 on his home purchase (this excludes property taxes and homeowners insurance).

SmartAsset

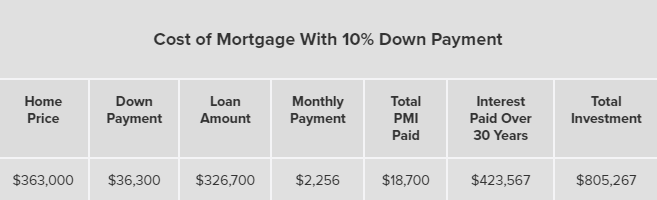

Tanya’s Approach: Put 10% Down and Invest the Rest

A table showing various aspects of a mortgage with a 10% down payment.

Putting 10% down on a $363,000 home means Tanya has to take out a larger loan ($326,700) and also pay $170 per month in PMI. The PMI payments will eventually end when she has repaid 22% of the home value, but they will add up to nearly $19,000 in total. After 30 years of making regular monthly payments, she will have spent an approximate total of $805,267 on the home.

SmartAsset

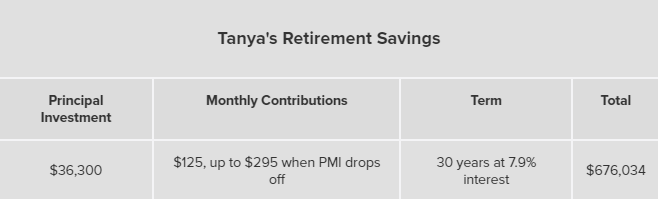

Tanya’s Retirement Savings

A table showing a projection of retirement savings.

By putting 10% down, Tanya has an extra $36,300 to invest in the stock market. Her monthly mortgage payment is also $125 less than it would be if she had opted for a 5% down payment. Assuming she invests that difference every month over the course of the 30-year period, here’s a look at how her money could grow:

Keep in mind that Tanya will pay PMI until she reaches the 22% equity threshold. At that point, her lender will automatically remove this monthly surcharge. This will happen early in the 10th year of her mortgage. From that point on, she’ll have an extra $170 freed up to invest each month for a total new monthly investment contribution of $295.

By reinvesting her PMI savings each month, Tanya’s investment portfolio would eventually grow to $677,361, assuming an average annual growth rate of 7.9%

SmartAsset

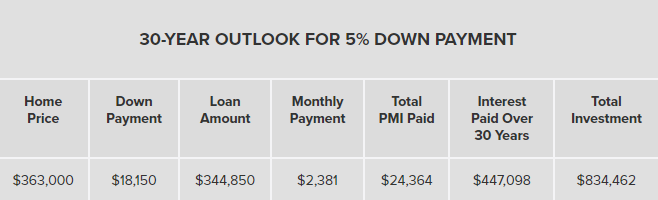

Frank’s Approach: Put 5% Down and Invest the Rest

A table showing various aspects of a mortgage with a 5% down payment.

Opting for a 5% down payment will leave Frank paying $2,202 each month toward his principal and interest, plus $179 in PMI. By the end of his 30-year mortgage, he will have paid an estimated $834,462 for his home.

Putting 5% down, however, allows Frank to immediately invest $54,450 in the stock market. Just keep in mind that his monthly mortgage payment will be higher so he won’t be able to make additional contributions to his investment account until PMI is removed.

SmartAsset

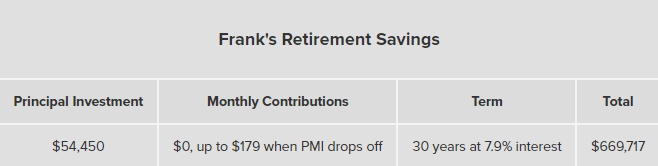

Frank’s Retirement Savings

A table showing a projection of retirement savings.

Putting only 5% down also means Frank pays PMI longer than Tanya. This monthly charge will disappear by the fifth month of his 12th year of repayment. At that point, he’ll have an extra $179 to invest each month.

As a result, Frank’s seed money will grow to nearly $670,000 by the time he pays off his mortgage, assuming the same 7.9% annual rate of return.

SmartAsset

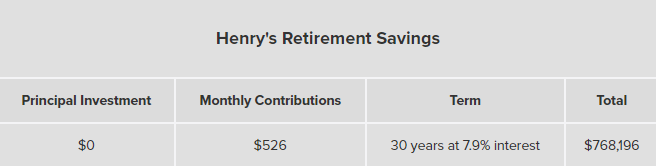

The Verdict

A table showing a projection of retirement savings.

At first glance, putting 10% down appears to make the most sense financially. While the 20% option means Henry ends up spending the least amount of money on his home ($739,504), the 10% strategy leaves Tanya with the largest nest egg ($677,360) by the time her home is paid off, plus PMI savings. So that settles it, right?

Not exactly.

Putting 20% down results in a monthly payment that’s $526 less than the 5% option. Rather than spend the extra money every month, Henry could use it to build up his retirement nest egg. Investing $526 each month would leave him with a whopping $768,196 after 30 years, assuming the same 7.9% growth rate. Not only would Henry save tens of thousands on his mortgage compared to Tanya and Frank, he’d also have a significantly larger investment portfolio at the end of the 30 years.

Lastly, today’s interest rate environment underscores the value of a 20% down payment. If interest rates were approximately 3%, as they were in 2021, the net difference between the three strategies would be significantly smaller. But with interest rates more than double what they were two years ago, the 20% option becomes the clear winner.

Then again, a smaller down payment offers a certain liquidity advantage over locking up all your cash in a home. Having more cash on hand may allow you to invest sooner in a home renovation or fully fund your emergency fund.

Should You Buy Now or Wait?

With interest rates twice as high as they were less than two years ago, prospective home buyers are wondering whether they should buy now or wait for rates to fall.

Waiting a year or so has several potential advantages. First, it will allow you to save up a larger down payment. Second, rates could come down in the next year, making your mortgage more affordable.

In December, the National Association of Realtors projected mortgage rates would fall to 5.7% in 2023 and the median sales price of existing homes would rise to $385,800.

How to Save Up for a Down Payment

Purchasing a home with a large down payment has obvious benefits. Here are some tips to help you save more and beef up your down payment.

Plan for closing costs. Closing costs include one-time, upfront costs when you take out a mortgage – usually between 2 and 6 percent of the loan amount.

Eliminate your debt. Paying off your outstanding debts will not only help you qualify for a larger mortgage, it will help you save up for your down payment faster.

Look into down payment assistance programs. A number of programs administered by state and local governments, as well as nonprofit organizations, are designed to provide extra cash to those who qualify.

Park your money in a high-yield account. Make sure your down payment is in a high-yield savings account and is earning well above the national average of just 0.13%. Some accounts have APYs of more than 4%.

Consider a starter home. If you don’t have enough savings to buy your forever home, consider buying a starter home now and trading up later. A mortgage calculator can help you understand what you can afford.

Bottom Line

Buying a home and investing in the stock market don’t need to be mutually exclusive. Whether you choose to make a 20%, 10% or 5% down payment, there are ways to invest your extra cash. After crunching the numbers, it’s clear that putting 20% down and investing your monthly savings is the best of the three strategies given the assumptions above. But keep in mind that macroeconomic conditions and local housing markets are always changing, which can affect your individual outcome.

This story was produced by SmartAsset and reviewed and distributed by Stacker Media.