How auto loans compare by generation

Canva

How auto loans compare by generation

Salesman Giving Key to Customers in Modern Auto Dealership

Auto loan data reveals some interesting insights about how consumers of different ages tend to finance their vehicles. Experian analyzed its consumer debt data to look at how the number of auto loans, average loan costs, and missed payments vary across generations.

One notable trend is that U.S. consumers born between 1965 and 1980 are more likely to have multiple auto loans. These Generation X vehicle owners also spend the most on average on monthly car bills compared with other age groups. And whether the vehicle is a workhorse pickup or a luxury convertible, data suggests that the older the vehicle owner is, the less likely they are to be making payments on it.

This pattern may also track with what is known about differences in wealth built by different generations. At the start of 2022, millennials still lagged behind the wealth levels accrued by Gen X and baby boomers when they were at the same points in their lives, according to data from the Federal Reserve Bank of St. Louis.

Generation Z and millennials, more likely than older generations to hold only a single auto loan, saw their average monthly auto payments increase the most of any generation year over year in 2022. Gen Zers are ages 9 to 25, and it’s too early to say how the financial habits of the group’s adult consumers—ages 18 to 25—will look. Younger Americans are more likely to borrow money for their automobile purchase than any other generation, according to the most recent Experian auto loan data. They’re also more likely to struggle with making car payments.

Of course, car owners of all ages have seen the cost of new vehicles skyrocket since spring 2021, triggered by a surge in demand amid computer chip shortages and other supply chain constraints. But even before the pandemic, sticker prices had been steadily rising. At the end of Q1 2013, the average cost of a new car was $31,526; by Q1 2022, it had climbed to $45,927, according to Kelley Blue Book.

As prices have increased, loan terms have been getting longer than ever, which has also played a role in changing auto loan habits. Read on to see how these trends have shaped the financial landscape for U.S. car owners across generations.

![]()

Experian

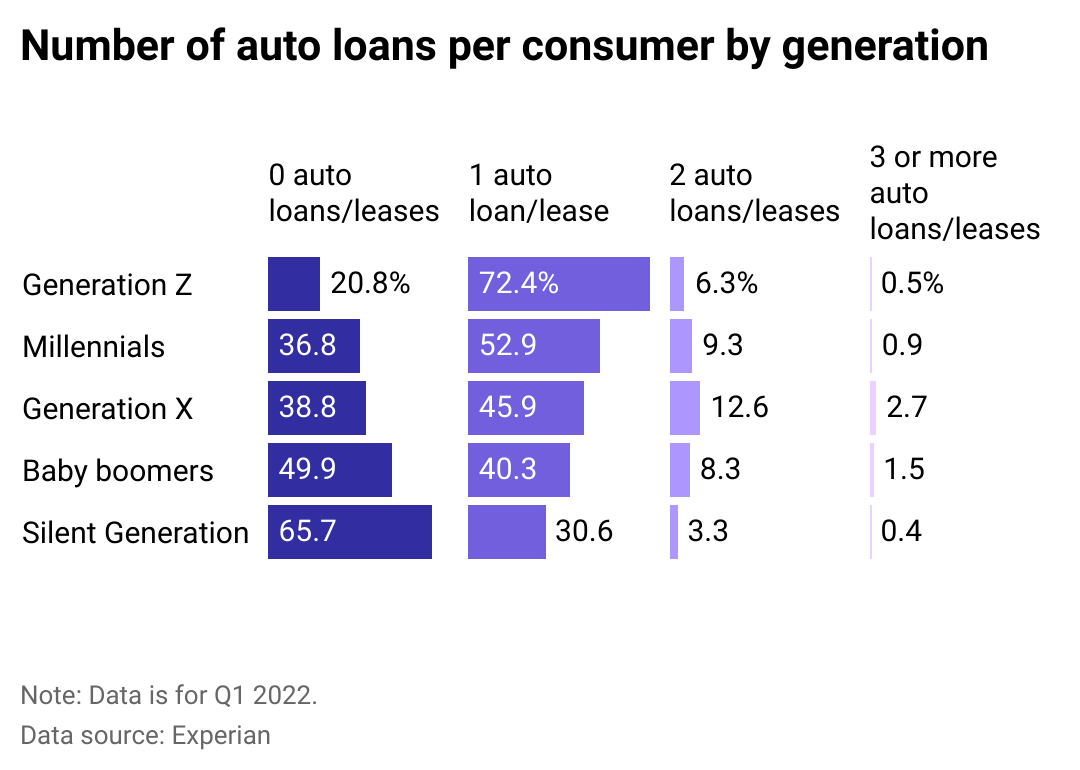

Older generations take out fewer car loans

Bar chart showing the number of auto loans per consumer by generation.

Members of the Silent Generation—born from 1928 to 1945—are the least likely to have an auto loan. About half of all baby boomers, a generation now in their 60s and 70s, are paying down at least one auto loan. This could indicate that older consumers are more likely to have paid off their auto loans and own their vehicles outright.

Older generations have generally had more time to build their wealth and pay off their debts, so it’s unsurprising that 4 in 5 members of Gen Z over age 18 hold at least one auto lease or car loan. As of 2022, the older members of Gen Z are reaching the age of 25, and are just getting their foothold in the workforce. But estimates of Gen Z’s purchasing power have jumped in recent years. This growing and diverse cohort of consumers saw their gross income jump nearly 40%—from $27,779 in 2019 to $38,635 in 2020—according to the Bureau of Labor Statistics.

Experian

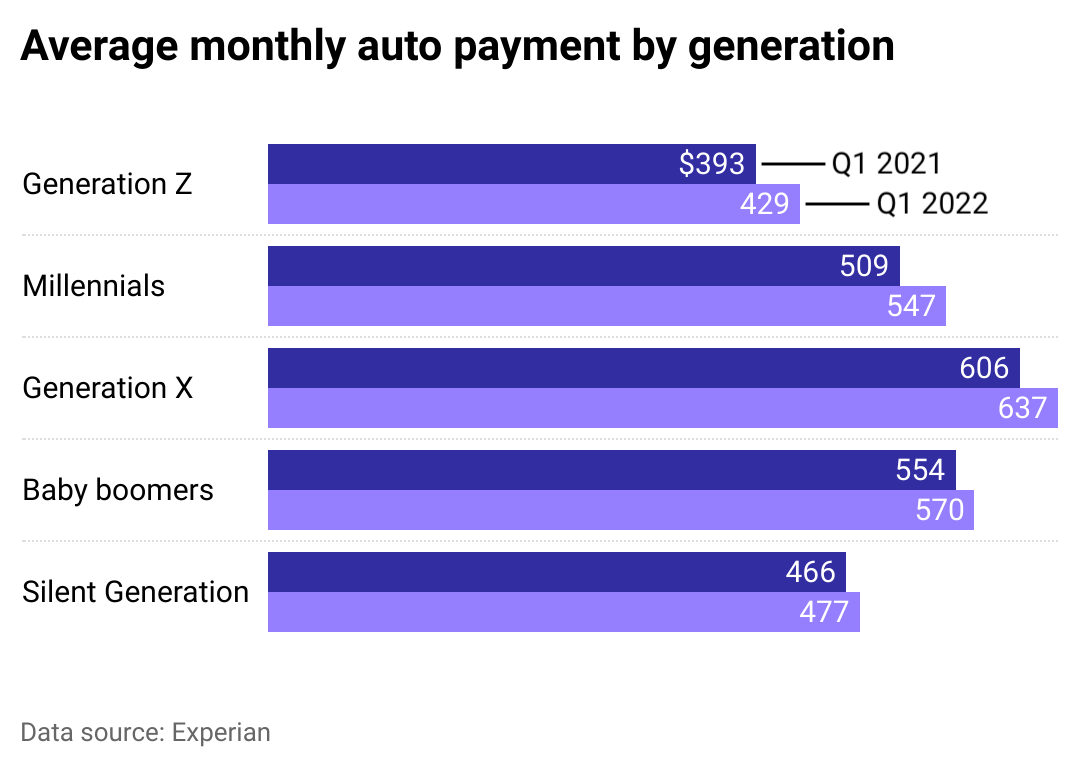

Gen X pays the most for monthly auto payments

Bar chart showing the average monthly auto payment by generation.

While millennials and Gen Zers are comparatively more likely to have an auto loan, it’s Gen X that is paying the biggest bills each month. Gen Xers are considered to be in their peak spending years and earned more income than any other generation in 2020, according to BLS data. These Americans may be financing more expensive vehicles than younger generations of consumers.

At the start of 2022, Gen X vehicle owners were paying $637 per month on average for their auto loans. That’s compared with $547 for millennials and $429 for Gen Z on average each month.

When it comes to the largest increase in their bills, Gen Z’s auto loan payments jumped 9.2% year over year between 2021 and 2022—a much bigger rise than other generations. Millennials followed behind them with a 7.5% jump over their 2021 average.

Experian

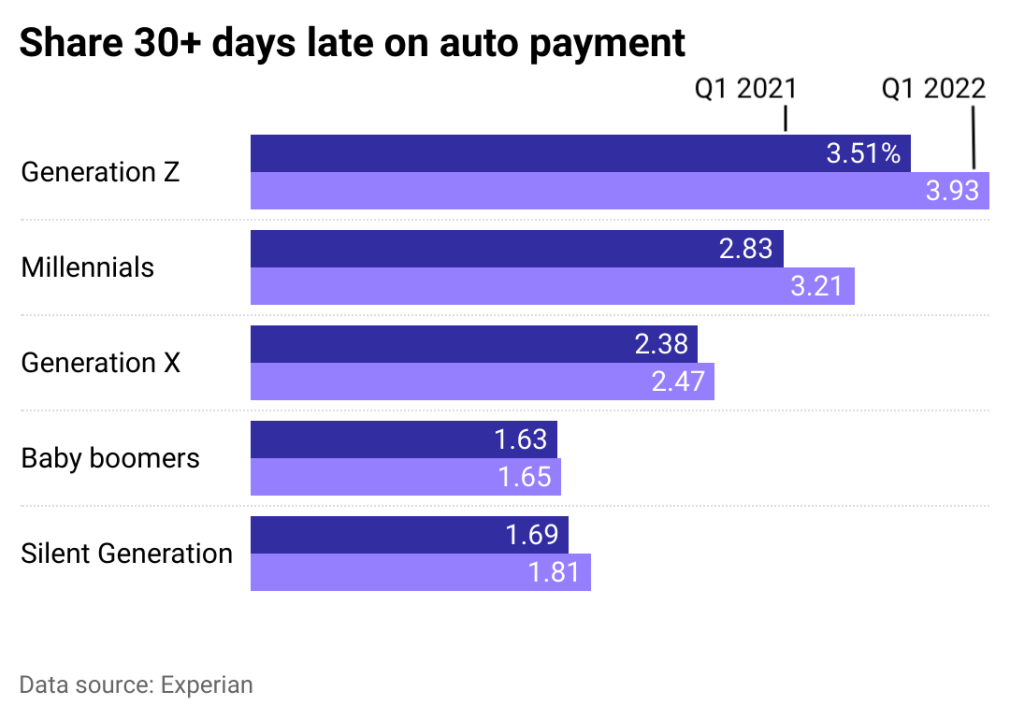

Gen Z has the highest share of late auto payments

Bar chart showing the percentage of each generation that is 30-plus days past due on auto payments.

Gen Zers are struggling the most of any generational cohort to keep up with auto loan payments. However, U.S. consumers of all generations had a harder time making timely payments on their auto loans at the start of 2022 compared with last year. Year-over-year increases in late payment rates were most dramatic for millennials and Gen Z auto owners; their incidence of individuals with currently late payments increased by 13.4% and 12%, respectively.

An auto loan is considered delinquent when a monthly payment is missed by 30 days or more. Lenders may not consider a loan in default until three payments in a row are missed, or payment is generally more than 90 days late. Repossession can occur after that length of time. The timeline for default and repossession can vary by lender, however.

This story originally appeared on Experian and was produced and

distributed in partnership with Stacker Studio.